It’s the midpoint of summer and a good time to catch up on “summer reading”. For us at Arkieva, that means digging into industry reports and predictions. Here are a few articles that recently caught our eye.

From the Wall Street Journal

We’ll begin with some good news. Wall Street Journal logistics writer Paul Berger wrote about a general easing of transportation costs. And given the huge spike in inflation this year, it is nice to see some costs decrease. Paul writes that, “Freight specialists say different forces are driving down rates across ocean shipping and trucking, but softening demand is a common factor. The lower rates are appearing first in spot markets and are helping to bring down longer-term contract rates.” And that, “One official at a large U.S. importer said it recently reduced by 15% to 20% ocean contract rates signed several months ago. The official expects further reductions later this year. “Things are trending in favor of the importers,” the official said.”

It remains to be seen whether this reduction in shipping costs translates to a reduction in costs to the consumer. It is more likely that the drop in shipping costs will net an easing on margin pressure. Consumers will still pay more than in the past, but inflation will flatten a bit.

Read the full article here.

From the Institute for Supply Management (ISM) Member Survey

Based on member surveys, ISM expects continual economic growth in the US through the remainder of the year. This is despite growing inflation and unrest in the world (globally the picture is less rosy). Specific bright spots are in manufacturing revenue. ISM reveals that “Revenue for 2022 is expected to increase, on average, by 9.2 percent. This is 2.7 percentage points higher than the December 2021 forecast of 6.5 percent, and 4.9 percentage points lower than the 14.1-percent year-over-year increase reported for 2021. Sixty-three percent of respondents say that revenues for 2022 will increase, on average, 15.5 percent compared to 2021. Only seven percent say revenues will decrease (10 percent, on average), and 30 percent indicate no change.”

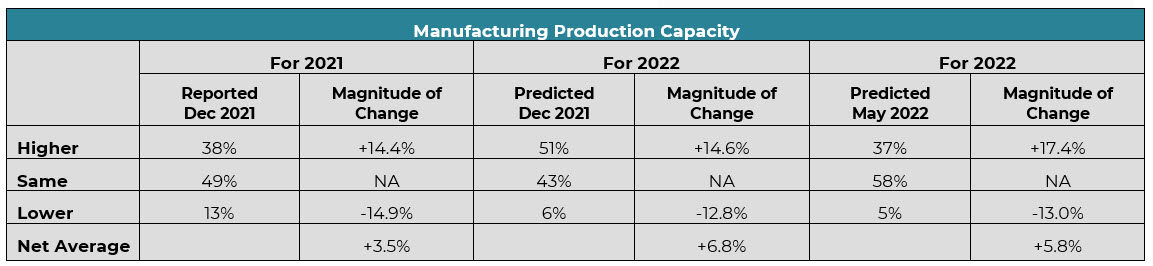

The second bright spot is on manufacturing capacity increasing. Respondents reported that “Production capacity is expected to increase 5.8 percent in 2022; in December, panelists reported an increase of 3.5 percent for 2021 and projected an increase of 6.8 percent this year. Thirty-seven percent of respondents expect capacity increase of, on average, 17.4 percent; 5 percent expect decreases of, on average, 13 percent; and 58 percent expect no change”.

Click to enlarge

The base of those who completed the survey represents a cross-section of industry leaders and doers. As a reader, it is useful to benchmark your own thoughts or concerns against the industry. From an Arkieva perspective, it confirmed a lot what we are hearing from our customers.

Read the full article here.

From the University of Rochester

However, increased production capacity, increased revenue and lower shipping costs will not translate to fewer supply chain problems. At least that is what University of Rochester economist George Alessandria says. He thinks that our current supply chain issues are “The worst that it’s been in 50 years—and it’s probably getting worse, considering that China has been shutting down cities and production facilities. The massive lockdowns in Shanghai and Beijing will eventually ripple through the system again.”

These “ripples” translate to increased chances for a recession. George adds, “There are so many things going on in the world right now that it’s hard to isolate one factor. But in our research, we found that these supply disruptions would lower economic activity by about one percentage point within six quarters of the start of the disruptions. So, the disruptions that we’re currently seeing could knock 4 to 5 percent off of industrial production in the next year or two, which is pretty substantial.”

Semiconductors are one area of great concern. With so much manufacturing capacity coming from the East, and China specifically, there is huge risk to supply. Especially if China decides to take action in Taiwan. Taiwan’s semiconductor manufacturing accounted for $115 billion, which is about 20% of the global semiconductor industry. Any disruption here will severely affect global economy. For example, even as this is being written in the summer of 2022, the auto industry will still not be back to normal until 12 to 18 months from now (The Morningstar link below has more details about semiconductor and other key industries).

Read the full University of Rochester article here.

From McKinsey and Company

McKinsey recently assembled several of their supply chain and operations leaders for a podcast on “Diagnosing the Pain in Your Supply Chain.” It covered several expected topics ranging from talent and pandemic lessons to inflation. However, the two most interesting points we heard were on the importance of the supply chain to the CEO. Don Swan, Mckinsey’s Global Coleader, Operations Practice, notes that, “Oftentimes in the past supply chain was what I would call a necessary evil. You needed your supply chain there to get product to your customer. And now, I think we see it more and more as a real differentiator for companies.”

The other comment was on the importance of scenario planning. This was called out by McKinsey Stuttgart Office Partner Knut Alicke, who said, “we also see companies that were early adopters of end-to-end planning processes, thinking in scenarios, also thinking in probabilities, that are doing better because they now have the options to compare different scenarios. Whereas other companies have struggled to even calculate a scenario and then have no alternative.” Scenario planning is near and dear to our hearts at Arkieva, and we fully agree with Knut’s comments. We’d also add that early adapters of end-to-end planning solutions have established case studies. This makes it easier for those that follow early adopters to make the business case for true end-to-end planning. The risk is moving from trying something “unproven” to waiting too long to make a strategic move.

Read the transcript of the podcast here.

From Morningstar

Lastly, Morningstar had a lengthy article on “Where does the Supply Chain Crisis Stand Now?” The report contains several thought-provoking charts on inventory levels, operating margins and revenue, and commodity pricing. This chart is a good representation of global disruptions.

Click to enlarge

There are deep dives on the automotive, food services, industrials and semiconductor industries in the article. Quite frankly there is not enough space to reference them all. We suggest you read the full report here.

There is a lot of useful information in these links. Even if all do not pertain to your industry, we are certain you will glean a good idea or two that can help you as we all push forward in these volatile times. If you have questions about your specific supply chain challenges, feel free to reach out. Our team is always available to connect with you.