Note: the full interview between Lora and Bram is available on Supply Chain Insights podcast.

I was recently interviewed as a blogger for the Global Summit. The question was how I imagine the Supply Chain in 2020. My first thought went to ‘deep integration’.

What strikes me the most when I’m consulting or teaching companies is the lack of integration in today’s supply chains. If I look at retailers it is still common to have private label suppliers stuffed with inventory, central or regional DC’s stuffed with inventory and shops stuffed with inventories. We all demand high service levels from one step to the next. There seems to be a lack of trust, a lack of transparency, a lack of integration. Seeing this, makes my supply chain heart weep. I was lucky to pursue a Phd in multi-echelon inventory optimization. It is easy to show that instead of buffering risks echelon per echelon, it is better to let go of internal service levels and pool risks on the customer facing echelon. Letting go of the internal service levels also allows optimization of costs and focuses the supply chain on the service level that really counts, which is the one to the final customer.

I see comparable things in B2B markets. We have outsourced big chunks of manufacturing but are stuck with inflexible supply contracts. We are exposed to tier-2 risks but are unaware and only discover it after the Japan earthquakes or the Thailand floods. We may sell our product via distributors, but they are often averse of keeping inventories, they demand short lead times and high service levels. Or we might sell directly to end customers, but we often have little to no view on their inventory levels, actual or planned consumptions. We just see spiky orders in an irregular pattern and have to deliver at +95% service levels. Again there seems to be a lack of trust, a lack of transparency, a lack of integration.

So why would it change?

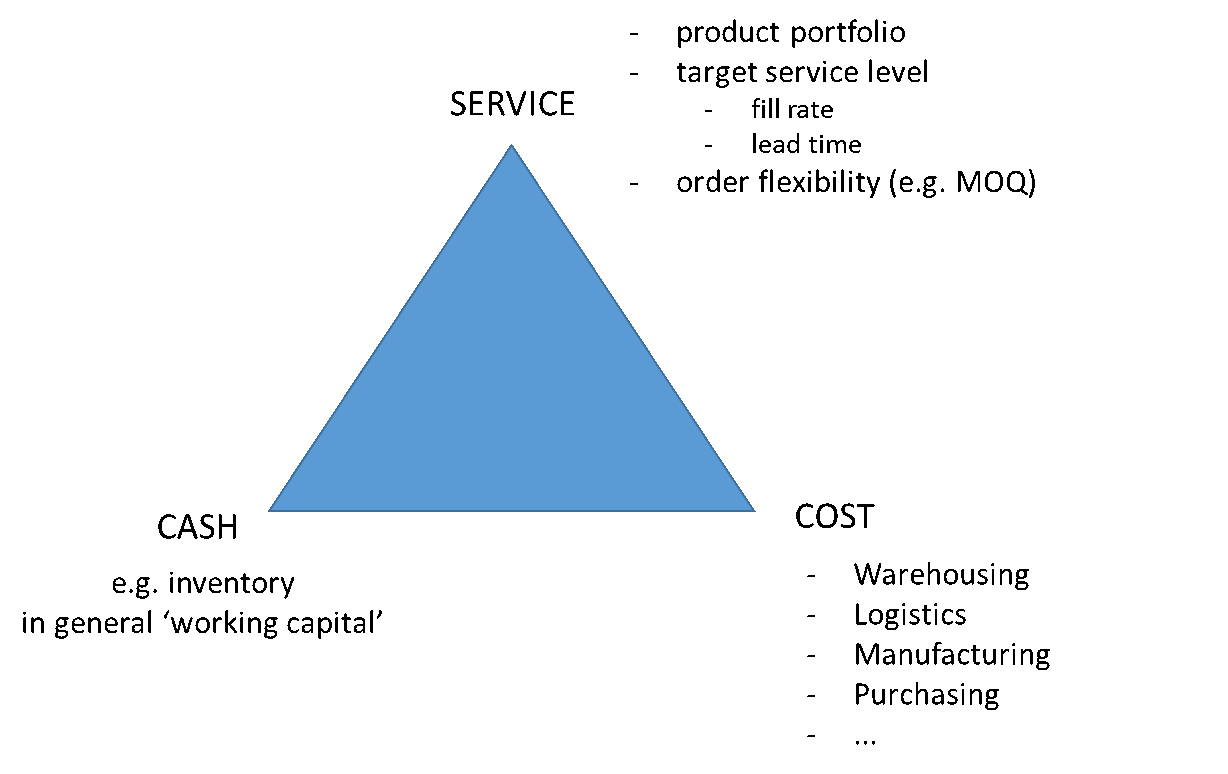

In recent projects and teachings I have often referred to the supply chain triangle as a concept to illustrate the basic trade-offs to be made in supply chain. It is shown below. One can imagine that increasing service by offering more products on a shorter lead time can increase both cash and cost. Sourcing in low cost countries could lower cost but increases inventories and inventory risk (write-offs).

In general, I believe that in the last decade, the pressure on cash, cost and service has been steadily increasing. The financial crisis of 2008-2009 has given a major push to do more with less. In retail the online players are putting the pressure on the brick-and-mortar players to improve service at reduced prices. In many B2B markets global flows have become the standard. Excess capacities in one region are dumped in another region and are disrupting market shares. To survive, inventories and margins need to be as sharp as a razor blade.

As the pressure on cash, cost and service keeps on rising, many companies will have no alternative to a deeper integration. To use Lora’s words they will need to become truly “market-driven”. Picking up demand signals down in the market and translating them to the upstream operations. But also picking up supply signals up in the supply markets and translating them into demand shaping actions down at the customer side. We will have to cross company borders, pushing stocks down the chain e.g. to distributors, and working out financing agreements that share the burden over all parties involved. We will have to account for production costs at the private label manufacturer, and see how we can efficiently plan the extended supply chain instead of just echelon per echelon.

What’s the biggest risk?

Technologies will have to evolve. Traditional integrated planning systems are going wall-to-wall but have difficulties crossing those walls. What to do if I have 50 distributors each using a different ERP developed by a local company in a local language?

Processes will have to adapt. Instead of having a commercial discussion with my distributor once every quarter, where they commit to orders, and where ordering behavior is driven by sales incentives and price reductions. We will need to come to daily or weekly monitoring and ordering and agree who will be financing which part of the inventories, who will take responsibility for non-movers, … We will need to do a true S&OP with our suppliers to show true market demands, assess the supply chain cost of up- and downswings, decide how to split the costs and the margins of the decisions we take.

But the biggest risk is certainly the trust. Purchasing may not like an open communication with the supplier as it undermines their negotiation position. Sales may distrust a supply chain way of managing channels as it limits their flexibility to hit targets. As Lora rightly mentioned in the interview, we’ll have to define what we mean with integration. And we’ll have to specify how the new, integrated model, is working compared to the old. We’ll need to show sales people how true demand shaping can help hitting targets while improving margins. We’ll have to show purchasing people how sharing information shifts the discussion from cost reduction to benefit sharing and how to deal with that type of discussions. We’ll have to build and advertise successful cases. Building these cases will require a team that has a broad end-to-end supply chain view. This will require horizontal career paths, ensuring sales has been in purchasing or manufacturing and vice versa. It will also require visionary leaders who have the vision and are ready to take the leap forward.

So it will depend on the people. Up to all supply chain believers to push the vision and translate it into manageable pieces. This will ensure we keep moving to the next level as we’re marching to 2020.